25 Things to Pack for a Cruise

25 Things to Pack for a Cruise

Okay, let’s talk about the annual benefits enrollment email from HR. You know the one. It’s filled with a million acronyms that all sound the same, and you’re just trying to figure out how to pay for your next dentist appointment without going broke. The biggest head-scratcher of them all? The difference between an HSA and an FSA.

They both let you use pre-tax money for medical expenses, which is amazing for saving cash. But they are NOT the same thing, and picking the wrong one can mean literally losing hundreds of dollars. No pressure!

Don’t worry, I sorted through the jargon for you. Here’s the real-deal breakdown of the difference between an HSA and an FSA, plus the accounts I actually think are worth opening.

Think of a Health Savings Account (HSA) as a personal savings account, but specifically for healthcare costs. It’s *your* money, in an account with *your* name on it. To get one, you absolutely must be enrolled in a high-deductible health plan (HDHP). No exceptions, sorry!

The best part? The money is yours forever. It rolls over every single year, so you never have to scramble to spend it in December. You can even invest the money in your HSA, kind of like a 401(k) for your health. It’s a legit long-term savings tool.

A Flexible Spending Account (FSA) is a bit different. This account is owned by your employer, not you. You decide how much money to put in at the beginning of the year, and it’s deducted from your paychecks pre-tax. You can use it for all the same qualified medical expenses, like co-pays, prescriptions, and even new glasses.

Here’s the catch, and it’s a big one: an FSA is “use it or lose it.” Most of the money you don’t spend by the end of the year just… disappears. Poof. Gone. Some companies offer a small rollover amount or a grace period, but you can’t just let that cash pile up for years like you can with an HSA.

So when you strip it all down, the main difference between an HSA and an FSA comes down to three things: ownership, rollovers, and eligibility.

An HSA is your personal property; it stays with you even if you change jobs. The money rolls over and grows indefinitely. But, you need that specific high-deductible health plan to even qualify.

An FSA is tied to your job. If you leave, you usually lose the account. The money expires at the end of the year. But, pretty much anyone with a job-based health plan can get one, which is super convenient.

If you’re on an HDHP, getting an HSA is a no-brainer. But not all accounts are created equal. Some have sneaky fees and terrible investment options. These are the ones that are actually good.

Fidelity’s HSA has a $0 annual fee. If you’re looking to actually grow your money and not just let it sit there, this is your best bet. I was seriously impressed by the return you get on just your uninvested cash alone.

They give you a ridiculous 3.37% APY on your cash balance, which is way more than most savings accounts right now. Plus, there are no account fees or investment fees, so every penny you save actually stays yours. It’s perfect for people who want to be hands-on with their investments.

The Downside: You have to be enrolled in a high-deductible health plan (HDHP) to open one. That’s the rule for all HSAs, but it’s still the biggest barrier.

Lively also has a $0 annual fee for individuals. This is the one I’d recommend to my friend who manages her entire life from her phone and wants something that just *works*.

The app is incredibly sleek and easy to use for tracking receipts and expenses. And for investing, it connects seamlessly with a Charles Schwab account, giving you tons of options without a complicated interface. User reviews are glowing for a reason—it’s just so user-friendly.

The Downside: It’s really built for individuals. If you’re an employer looking for a solution for your whole team, you might need to look elsewhere.

There’s a $0 monthly fee here. HSA Bank is a solid, middle-of-the-road option that gets the job done without any fuss. It’s not the flashiest, but it’s reliable and straightforward.

It’s a good balance if you want to keep some money in cash for upcoming appointments but also invest a little for the future. They have thousands of self-directed investment options, so you can really customize your portfolio once your balance is high enough.

The Downside: They do charge investment fees, but those get waived if you have over $7,500 in your investment account. It’s a bit of a bummer for small-balance investors.

The annual fee here can be anywhere from $0 to $60, depending on your balance and your employer’s plan. This is a huge player in the corporate world, so there’s a good chance you might be offered this one through your job.

HealthEquity is built to handle everything for big companies, which is great for HR departments. It can manage HSAs, FSAs, and other benefits all in one place. For users, you get a debit card and some decent analytics tools to track your spending.

The Downside: The user reviews are… not great. Their Trustpilot score is a scary 1.0/5, with lots of complaints about customer service. You might not have a choice if your employer uses them, but just be aware.

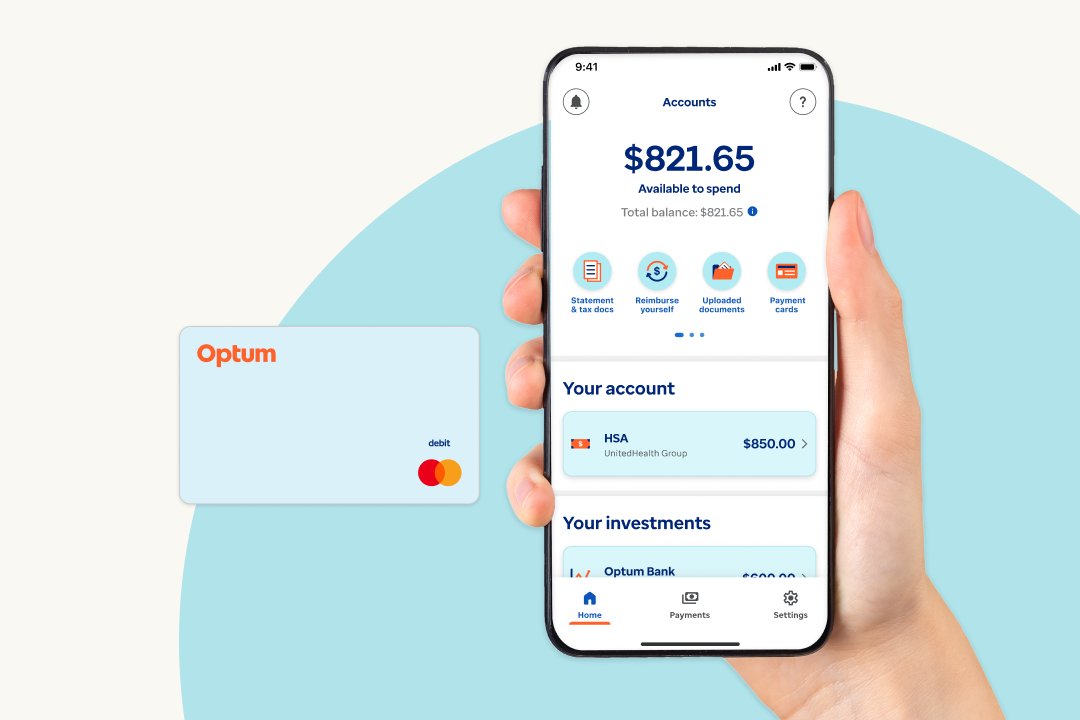

This one costs about $2.75 a month, but your employer often covers it. If you have a UnitedHealthcare insurance plan, getting the Optum Bank HSA just makes life so much easier.

Everything is integrated, so your claims and payments talk to each other seamlessly. The mobile app is solid for managing reimbursements, and you get access to a Schwab brokerage account for investing. It’s designed for people who are actually using their health insurance often.

The Downside: If you don’t meet the minimum balance requirement, you’ll get hit with fees. It’s definitely best for people whose employers are footing the bill.

The fee is $2.50 per month, which works out to $30 a year. If you’re already a Bank of America customer, the convenience factor here is huge. You can see your HSA right next to your checking and savings accounts in one app.

You get a Visa debit card and access to Merrill mutual funds for investing. I liked that I could just pull cash from any BofA ATM if I needed to for a reimbursement. It’s a very traditional banking experience, which can be comforting.

The Downside: There’s a monthly maintenance fee. In a world with so many fee-free options like Fidelity and Lively, paying a fee feels a little outdated unless the convenience is a top priority for you.

This account has a $0 annual fee. It’s a simple, no-frills option for anyone who wants an HSA without paying for it and doesn’t need intense investment features.

It’s perfect if you plan to keep a lower balance and just use it to pay for current medical bills. You get a free debit card, online tools that are easy to figure out, and you won’t be dinged by maintenance fees. It does what it says on the tin.

The Downside: The interest you earn on small balances is basically nothing (like 0.01%). You need a pretty high balance to start earning their more competitive rates.

Pricing is custom for employers. You probably won’t be signing up for Forma as an individual, but you might see it offered through a modern, tech-forward company.

Forma puts all of a company’s pre-tax benefits—HSA, FSA, commuter benefits, you name it—into one clean platform. It’s designed to make it super easy for employees to actually use their benefits, which is a huge plus. The dashboard is great for keeping track of everything.

The Downside: It’s really an enterprise product. If you’re a freelancer or your company doesn’t use it, you can’t get it.

So, which one should you choose? If you have a high-deductible health plan and want to build savings for the future, an HSA is 100% the way to go. The tax benefits and investment growth potential are just too good to pass up.

But if you don’t qualify for an HSA, an FSA is still an awesome tool. It’s perfect for predictable costs you know you’ll have in 2026, like therapy co-pays, contact lenses, or that pricey prescription. Just be realistic about how much you’ll spend so you don’t lose your hard-earned cash.

Either way, you’re saving money on taxes, which is always a win. Now go ace your open enrollment and spend that extra cash on something way more fun than a doctor’s bill.

25 Things to Pack for a Cruise

Shop Pop Mart Crybaby On Amazon

50 Best Organization Products to Declutter Your Home and Life

12 Best Bike Storage Ideas